This article provides a detailed look at student loan forgiveness programs available in 2026, outlining eligibility, application processes, and future opportunities for borrowers seeking debt relief.

Por: Marcelle em 27 de fevereiro de 2026

Anúncios

Student loan forgiveness programs in 2026 offer crucial relief through various federal initiatives, including income-driven repayment adjustments, public service opportunities, and targeted debt cancellation for eligible borrowers.

Understanding the Current Landscape of Student Loan Forgiveness

The student loan environment is ever-evolving, with significant changes and new initiatives frequently introduced. As we look towards 2026, it is vital for borrowers to understand the foundational programs that remain in place, alongside any new developments. These programs are designed to offer relief to individuals who meet specific criteria, often tied to income, profession, or particular circumstances.

Many borrowers often feel lost amidst the jargon and varying requirements of different forgiveness plans. The key is to identify which program best aligns with one’s personal and professional situation. Federal student loans, unlike private loans, are typically eligible for these government-backed forgiveness initiatives, making it crucial to distinguish between the two.

Anúncios

Key Federal Forgiveness Programs Still Active

Several long-standing federal programs continue to provide pathways to loan forgiveness. These include options for those in public service, educators, and individuals facing financial hardship. Understanding the nuances of each can significantly impact a borrower’s strategy.

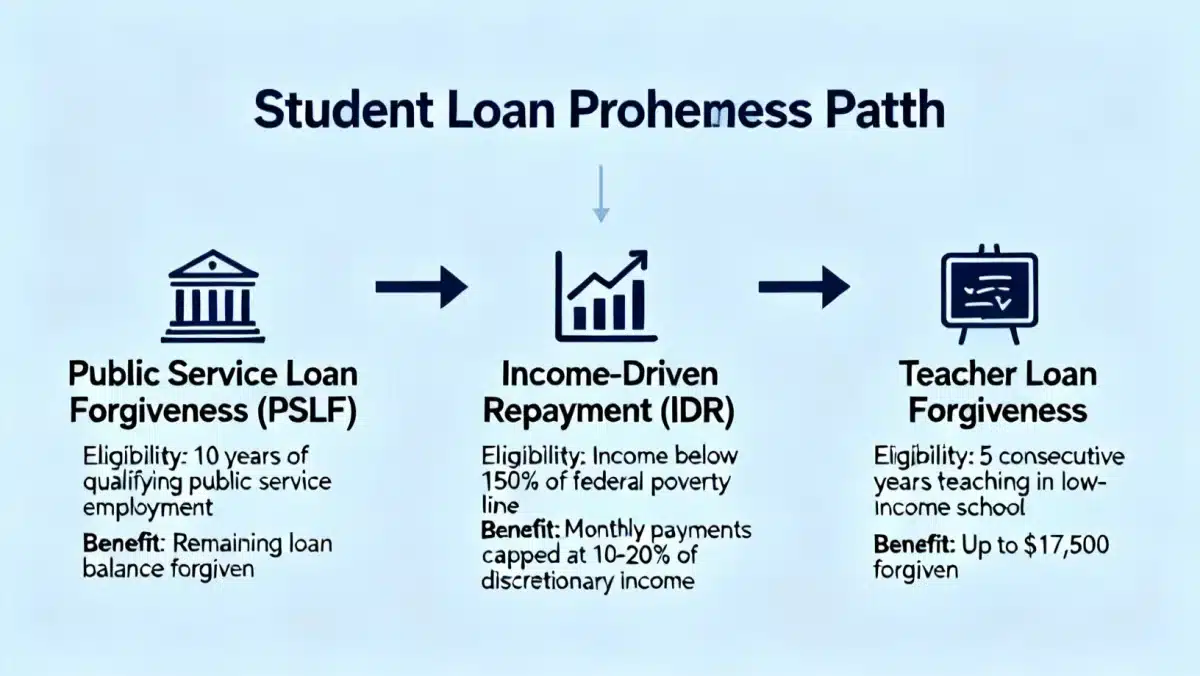

Public Service Loan Forgiveness (PSLF): Designed for full-time employees of government or not-for-profit organizations after 120 qualifying payments.

Teacher Loan Forgiveness (TLF): Offers up to $17,500 in forgiveness for eligible teachers who work for five consecutive years in low-income schools or educational service agencies.

Income-Driven Repayment (IDR) Forgiveness: After 20 or 25 years of payments on an IDR plan, any remaining balance is forgiven, though it may be taxable.

Beyond these, there are specific programs for borrowers with disabilities, or those whose schools closed. Each program has intricate eligibility requirements and specific application processes that must be followed meticulously. Staying informed about program updates and deadlines is paramount to successfully applying for and receiving forgiveness.

In summary, the current landscape of student loan forgiveness programs offers multiple avenues for relief, primarily for federal loan borrowers. It requires careful review of individual circumstances and diligent adherence to program guidelines to maximize the chances of successful debt cancellation.

Exploring Anticipated Changes and New Initiatives for 2026

The student loan landscape is not static, and 2026 is expected to bring further refinements and potentially new programs. Policymakers continuously evaluate the effectiveness of existing initiatives and propose new solutions to address the ongoing student debt crisis. Keeping abreast of these potential changes is crucial for proactive financial planning.

Recent years have seen substantial discussions about broad-based forgiveness and adjustments to existing IDR plans. While some proposals may not materialize, others could significantly alter the options available to borrowers. These discussions often revolve around making forgiveness more accessible, simplifying application processes, and providing more immediate relief.

Potential Policy Shifts and Program Enhancements

Future policy changes could impact various aspects of student loan repayment and forgiveness. These might include modifications to eligibility criteria, adjustments to payment thresholds, or even new categories of eligible borrowers. The aim is often to streamline the process and reduce administrative burdens for both borrowers and servicers.

Streamlined IDR Plans: Efforts are underway to simplify IDR plans, potentially reducing the number of plans and making them easier to understand and enroll in.

Expanded PSLF Eligibility: Discussions may continue regarding expanding PSLF to include more types of public service or to count more payment types towards the 120-payment requirement.

Targeted Debt Relief: There could be continued focus on targeted relief for specific groups, such as low-income borrowers or those who attended predatory institutions.

It’s also worth noting that the political climate plays a significant role in the implementation of new policies. Changes in administration or legislative priorities can either accelerate or slow down the introduction of new forgiveness initiatives. Therefore, borrowers should monitor reputable news sources and official government announcements closely.

In conclusion, 2026 could be a year of significant evolution for student loan forgiveness programs. Borrowers should remain vigilant and informed about any proposed or enacted changes that could benefit their financial situation.

Eligibility Requirements and Application Processes

Understanding who qualifies for student loan forgiveness and how to apply is often the most challenging part for borrowers. Each program has distinct requirements, and missing a single detail can lead to a rejected application. A thorough review of eligibility criteria and a meticulous approach to the application are essential.

General eligibility often hinges on the type of loan, the borrower’s employment, income level, and repayment history. Federal Direct Loans are typically the most eligible, while FFEL Program loans and Perkins Loans may require consolidation into a Direct Loan to qualify for certain forgiveness options.

Navigating Specific Program Requirements

While general principles apply, the specifics of each program demand careful attention. For instance, PSLF requires specific employment and payment types, whereas IDR forgiveness relies on consistent payments over a long period.

The application process also varies. PSLF requires annual certification of employment and a final application for forgiveness, while IDR plans are enrolled in through your loan servicer, with annual income recertification. It’s crucial to keep meticulous records of all payments and employment verification.

Loan Type: Ensure your loans are federal Direct Loans or have been consolidated into one.

Employment: Verify your employer qualifies for programs like PSLF or TLF.

Payment History: Track qualifying payments accurately for IDR and PSLF.

Income Documentation: Provide accurate income information for IDR plans annually.

Many borrowers make the mistake of assuming they are ineligible without fully exploring the options. It is always advisable to contact your loan servicer or the Federal Student Aid office for personalized guidance. They can provide clarity on your specific loan types and help you understand your eligibility for various programs.

To summarize, successful application for student loan forgiveness in 2026 depends on a clear understanding of eligibility criteria and diligent completion of the application process. Proactive engagement with loan servicers and careful record-keeping are key.

The Role of Income-Driven Repayment Plans in Forgiveness

Income-Driven Repayment (IDR) plans are a cornerstone of federal student loan repayment, offering a safety net for borrowers whose incomes are low compared to their student loan debt. Beyond making monthly payments more manageable, IDR plans serve as a direct pathway to loan forgiveness after a specified period.

These plans calculate monthly payments based on a borrower’s income and family size, ensuring that payments are affordable. There are several IDR plans, including SAVE, PAYE, IBR, and ICR, each with slightly different formulas for calculating payments and varying repayment periods before forgiveness. Forgiveness under IDR typically occurs after 20 or 25 years of qualifying payments, depending on the plan and whether the loans were for undergraduate or graduate study.

Understanding IDR Plan Mechanics and Forgiveness

The mechanics of IDR plans are designed to protect borrowers from default while steadily moving them towards a debt-free future. Any remaining balance at the end of the repayment term is forgiven. While this forgiveness can be a significant relief, it’s important to note that the forgiven amount may be considered taxable income by the IRS, unless Congress acts to extend the current tax-free status.

Affordable Payments: Monthly payments are capped at a percentage of your discretionary income.

Interest Subsidies: Some IDR plans offer interest subsidies to prevent your balance from growing excessively when payments are low.

Forgiveness Timeline: Forgiveness typically occurs after 20-25 years of qualifying payments.

Annual Recertification: Borrowers must recertify their income and family size annually to remain on an IDR plan.

The SAVE plan, a newer IDR option, is particularly noteworthy for its potentially more generous terms, including lower payment percentages and more substantial interest subsidies. Borrowers should evaluate whether switching to the SAVE plan or another IDR option would be beneficial for their long-term financial health and forgiveness prospects.

In essence, IDR plans are not just about managing monthly payments; they are a critical component of the student loan forgiveness strategy for many. Understanding their structure and actively managing your enrollment can lead to substantial debt relief in 2026 and beyond.

Specialized Forgiveness Programs and Targeted Relief

Beyond the broad categories of PSLF and IDR, several specialized programs offer targeted student loan forgiveness for specific professions or circumstances. These programs recognize the unique contributions of certain individuals or address particular hardships, providing tailored relief options.

For example, healthcare professionals, attorneys, and individuals working in underserved communities may qualify for specific state or federal programs. These often come with service commitments in exchange for partial or full loan cancellation. It’s crucial for borrowers in these fields to research all available options, as they can significantly reduce their debt.

Niche Forgiveness Opportunities

These niche programs often fill gaps where broader forgiveness options might not apply or might not offer the most advantageous terms. They are typically less known but can be incredibly impactful for those who qualify.

Perkins Loan Cancellation: For certain professions, such as teachers, nurses, and law enforcement officers, a portion of Perkins Loans can be cancelled.

Total and Permanent Disability (TPD) Discharge: Borrowers who are totally and permanently disabled may qualify for their federal student loans to be discharged.

Borrower Defense to Repayment: Forgiveness for borrowers whose schools engaged in misconduct or defrauded them.

Closed School Discharge: If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for discharge.

Additionally, some states offer their own loan repayment assistance programs (LRAPs) for professionals who commit to working in high-need areas within the state. These programs can often be combined with federal forgiveness options, amplifying the total relief received. Researching state-specific programs is a valuable step for many borrowers.

In conclusion, specialized forgiveness programs provide crucial relief for specific groups and situations. Borrowers should diligently explore all targeted options relevant to their profession or circumstances to maximize their chances of debt cancellation.

Strategic Planning for Student Loan Forgiveness in 2026

Successfully navigating student loan forgiveness programs in 2026 requires more than just knowing about the options; it demands strategic planning and consistent execution. Borrowers must be proactive in managing their loans, understanding their eligibility, and preparing for future changes. This involves regular review of loan statuses, communication with servicers, and staying informed about policy updates.

A well-thought-out strategy can significantly improve the likelihood of achieving forgiveness. This includes choosing the right repayment plan, meticulously tracking qualifying payments, and ensuring all necessary documentation is submitted on time. Ignoring these details can lead to delays or even disqualification from programs.

Key Steps for Proactive Loan Management

Effective management of your student loans involves several critical steps. These steps are not one-time actions but rather ongoing practices that ensure you remain on track for forgiveness.

Consolidate Loans if Necessary: Ensure all eligible loans are consolidated into a Direct Loan to qualify for federal forgiveness programs.

Choose the Right IDR Plan: Select the IDR plan that best fits your financial situation and long-term goals.

Track Payments and Employment: Keep detailed records of all payments made and employment certifications for PSLF.

Annual Recertification: Do not miss annual income and family size recertifications for IDR plans.

Stay Informed: Regularly check official government websites and reputable news sources for updates on programs.

Consider seeking advice from a qualified financial advisor specializing in student loans. They can offer personalized guidance, help you understand complex regulations, and assist in developing a tailored strategy for your specific situation. Their expertise can be invaluable in optimizing your path to forgiveness.

Ultimately, strategic planning for student loan forgiveness in 2026 involves a combination of informed decision-making, diligent record-keeping, and continuous engagement with your loan servicer and relevant government agencies. Proactivity is your greatest asset in this journey.

Key Program

Brief Description

PSLF

Forgiveness for government and non-profit employees after 120 qualifying payments.

IDR Forgiveness

Remaining balance forgiven after 20-25 years of income-driven payments.

Teacher Loan Forgiveness

Up to $17,500 for eligible teachers in low-income schools.

Targeted Discharges

Relief for disability, school closure, or institutional misconduct.

Frequently Asked Questions About Student Loan Forgiveness in 2026

What is the Public Service Loan Forgiveness (PSLF) program?▼

PSLF offers forgiveness for federal student loans after 120 qualifying monthly payments while working full-time for a U.S. federal, state, local, or tribal government or a not-for-profit organization. It is designed to incentivize public service careers. Eligibility requires specific loan types and repayment plans.

Are private student loans eligible for forgiveness programs?▼

Generally, private student loans are not eligible for federal student loan forgiveness programs. These programs are specifically designed for federal loans issued by the U.S. Department of Education. Private loan borrowers should contact their lender for any available relief options, which are typically limited.

How do Income-Driven Repayment (IDR) plans lead to forgiveness?▼

IDR plans calculate monthly payments based on your income and family size. After 20 or 25 years of qualifying payments, any remaining balance on your federal student loans is forgiven. Borrowers must recertify their income and family size annually to remain eligible for these plans.

Will forgiven student loan debt be taxable in 2026?▼

Currently, certain forgiven federal student loan debt is temporarily tax-free through December 31, 2025, due to the American Rescue Plan. Without further legislative action, forgiven amounts in 2026 and beyond could be considered taxable income by the IRS, so it’s important to monitor updates.

What should I do if I think I qualify for forgiveness?▼

If you believe you qualify for student loan forgiveness, the first step is to contact your federal loan servicer. They can provide specific details about your loans, explain eligible programs, and guide you through the application process. Always keep detailed records of your communications and submissions.

Conclusion

As we’ve explored, the landscape of student loan forgiveness programs in 2026 offers a variety of avenues for relief, from long-standing federal initiatives like PSLF and IDR to more specialized options. Understanding these programs, their eligibility requirements, and the application processes is not merely an academic exercise; it’s a critical step toward achieving financial stability and reducing the burden of educational debt. Proactive engagement, diligent record-keeping, and staying informed about potential policy changes are essential components of a successful strategy. While the journey to forgiveness can be complex, the opportunities available provide genuine hope for many borrowers seeking to alleviate their student loan obligations.