QBI Deduction Changes in 2025: Impact on Pass-Through Entities

Por: Gabrielle em 18 de setembro de 2025

Anúncios

Proposed changes to the Qualified Business Income (QBI) deduction in 2025 could significantly impact the tax liabilities of pass-through entities, potentially altering how income is calculated and taxed for many businesses.

Understanding how proposed changes to the **Qualified Business Income (QBI) deduction in 2025 affect pass-through entities’ tax liabilities** is crucial for business owners and tax professionals alike. These changes could reshape financial planning and tax strategies for many businesses.

Understanding the Current QBI Deduction

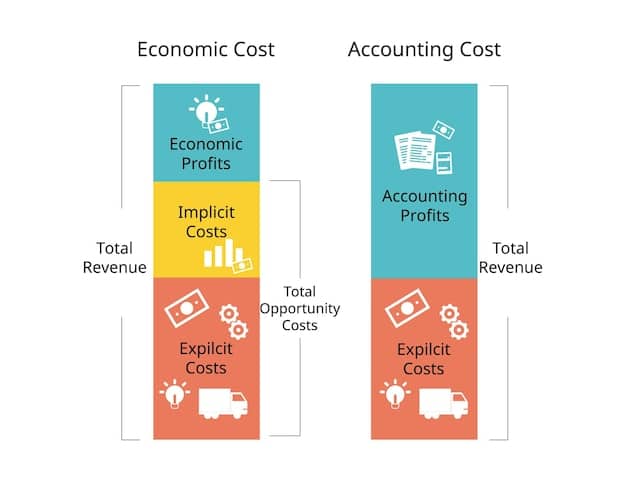

The Qualified Business Income (QBI) deduction, established by the Tax Cuts and Jobs Act of 2017, allows eligible self-employed and small business owners to deduct up to 20% of their qualified business income. This valuable deduction helps to reduce the tax burden on pass-through entities.

Eligibility Criteria

To be eligible for the QBI deduction, taxpayers must meet specific income thresholds and business requirements.

Anúncios

Taxpayers must own a qualified business, which generally includes any trade or business other than a C corporation.

The QBI deduction is subject to limitations based on taxable income. For 2023, the deduction is fully available for those with taxable income below \$182,100 (single) or \$364,200 (married filing jointly).

Specified Service Trades or Businesses (SSTBs), such as law, accounting, and consulting firms, have additional restrictions.

Calculating the Deduction

Calculating the QBI deduction involves several steps to ensure accuracy and compliance.

Identify the qualified business income, which includes net income, gains, and deductions from a qualified business.

Determine the applicable limitations based on taxable income and SSTB status.

Calculate the deduction, which is the lesser of 20% of QBI or 20% of the taxpayer’s taxable income (without regard to the QBI deduction).

Overall, the current QBI deduction offers significant tax relief to eligible pass-through entities and small business owners. Understanding the eligibility requirements and proper calculation methods is essential for maximizing these benefits.

Anticipated Changes to the QBI Deduction in 2025

As the provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 are set to expire in 2025, significant changes to the QBI deduction are anticipated. These changes could have far-reaching implications for pass-through entities and their tax planning strategies.

Sunset Provisions of the TCJA

The TCJA included several temporary provisions that are scheduled to expire after 2025, commonly referred to as sunset provisions. These provisions impact various aspects of the tax code, including individual income tax rates, deductions, and credits.

The sunset of these provisions means that unless Congress acts to extend or modify them, the tax laws will revert to those in place before the TCJA was enacted. This reversion could lead to higher tax rates and reduced deductions for many taxpayers.

Potential Scenarios for the QBI Deduction

Several potential scenarios could unfold regarding the future of the QBI deduction.

Full Extension: Congress could choose to extend the QBI deduction in its current form, providing certainty for businesses and taxpayers.

Modification: The deduction could be modified, with changes to eligibility criteria, deduction amounts, or other provisions.

Expiration: The QBI deduction could be allowed to expire, reverting to pre-TCJA tax laws.

Understanding these potential scenarios is crucial for businesses and tax professionals to prepare for future tax planning and compliance.

In summary, the anticipated changes to the QBI deduction in 2025 hinge on the sunset provisions of the TCJA and the actions taken by Congress. The ultimate outcome will significantly affect the tax liabilities of pass-through entities.

Impact on Different Types of Pass-Through Entities

The proposed changes to the QBI deduction in 2025 will not affect all pass-through entities equally. The specific impact will vary depending on the type of entity, its income level, and the nature of its business.

S Corporations

S corporations are pass-through entities where profits and losses are passed through directly to the owners’ individual income tax returns. Owners pay tax on their share of the corporation’s earnings.

Changes to the QBI deduction could significantly influence the amount of income that S corporation shareholders can deduct, directly affecting their tax liabilities.

Partnerships

Partnerships, including limited liability partnerships (LLPs) and limited partnerships (LPs), operate similarly to S corporations in that profits and losses pass through to the partners.

The variability in partners’ income levels and the partnership’s overall business income means that alterations to the QBI could disproportionately affect certain partners.

Sole Proprietorships

Sole proprietorships are the simplest form of business, where the business is owned and run by one person, and there is no legal distinction between the owner and the business.

Since sole proprietors report business income and expenses on their personal income tax returns, fluctuations in QBI eligibility and deduction amounts will impact their overall tax burden.

In conclusion, changes to the QBI deduction in 2025 will create varied outcomes for different pass-through entities. S corporations, partnerships, and sole proprietorships all face unique challenges and opportunities depending on their specific circumstances.

Strategies for Pass-Through Entities to Prepare

To navigate the potential changes to the QBI deduction in 2025, pass-through entities should consider implementing proactive strategies. These strategies can help mitigate potential tax increases and optimize financial planning.

Reviewing Current Tax Planning

A comprehensive review of current tax planning strategies is the first step in preparing for the future.

Assess current eligibility for the QBI deduction to understand the baseline.

Evaluate the impact of potential changes on taxable income and overall tax liabilities.

Identify areas for improvement or adjustment in business operations and financial structures.

Adjusting Business Structures

Depending on the nature of the business, adjustments to the business structure might be beneficial.

Consider restructuring to optimize QBI eligibility and maximize deduction potential.

Evaluate the benefits of converting from one type of pass-through entity to another.

Consult with legal and tax professionals to ensure compliance and alignment with long-term goals.

Forecasting and Modeling

Implementing forecasting and modeling techniques can help businesses anticipate and prepare for different scenarios.

Develop financial models that incorporate various potential changes to the QBI deduction.

Estimate the impact on cash flow, profitability, and investment decisions.

Use scenario planning to prepare for different outcomes and adjust strategies accordingly.

By actively reviewing tax planning, adjusting business structures, and implementing forecasting techniques, pass-through entities can better prepare for the potential changes to the QBI deduction in 2025.

The Role of Tax Professionals

Tax professionals play a critical role in helping pass-through entities navigate the complexities of the QBI deduction, especially with the anticipated changes in 2025. Their expertise and guidance can be invaluable in optimizing tax strategies.

Importance of Expert Guidance

Seeking expert guidance from qualified tax professionals is essential for pass-through entities.

Tax professionals are well-versed in the intricacies of tax law and can provide tailored advice based on the specific circumstances of each business. They can help businesses understand the implications of proposed changes and develop effective tax planning strategies.

Choosing the Right Tax Advisor

Selecting the right tax advisor is crucial for ensuring effective tax planning and compliance.

When selecting a tax advisor, consider their experience, qualifications, and expertise in pass-through entity taxation. Look for professionals who stay up-to-date with the latest tax laws and regulations.

Ongoing Support and Compliance

Tax professionals provide ongoing support and compliance services to help businesses stay on track.

Assistance with tax preparation and filing to ensure accuracy and compliance.

Regular updates on tax law changes and their potential impact.

Support in navigating audits and resolving tax-related issues.

In summary, tax professionals offer essential guidance and support for pass-through entities preparing for the proposed changes to the QBI deduction in 2025. Their expertise helps businesses optimize tax strategies, ensure compliance, and navigate complex tax regulations.

Long-Term Financial Planning Considerations

The proposed changes to the QBI deduction in 2025 underscore the importance of long-term financial planning for pass-through entities. Developing a comprehensive financial plan can help businesses adapt to changing tax laws and achieve their long-term goals.

Integrating Tax Planning with Financial Goals

Integrating tax planning with overall financial goals is essential for maximizing business success.

Tax planning should not be viewed in isolation but rather as an integral part of the broader financial strategy. Aligning tax strategies with financial goals ensures that businesses are making informed decisions that support their long-term objectives.

Investment Strategies

Adjusting investment strategies can help mitigate the impact of potential tax increases.

Consider tax-advantaged investment options to reduce overall tax liabilities.

Evaluate the timing of investments and disposals to optimize tax outcomes.

Diversify investments to minimize risk and maximize returns.

Retirement Planning

Comprehensive retirement planning is crucial for business owners.

Assess the impact of tax changes on retirement savings and income.

Adjust retirement plans to ensure adequate funding and tax efficiency.

Consider various retirement account options, such as SEP IRAs, SIMPLE IRAs, and 401(k) plans.

In conclusion, long-term financial planning is essential for pass-through entities navigating the potential changes to the QBI deduction in 2025. Integrating tax planning with financial goals, adjusting investment strategies, and developing comprehensive retirement plans can help businesses achieve long-term financial success and stability.

Key Point

Brief Description

📝 QBI Deduction

Allows deduction of up to 20% of qualified business income.

Impacts S corps, partnerships, and sole proprietorships differently.

🛡️ Preparation

Review tax plans, adjust structures, and forecast scenarios.

FAQ

What is the QBI deduction?▼

The QBI deduction allows eligible self-employed and small business owners to deduct up to 20% of their qualified business income, reducing their overall tax liability and fostering economic growth.

When are changes expected to the QBI deduction?▼

Significant changes to the QBI deduction are anticipated in 2025 due to the sunset provisions of the Tax Cuts and Jobs Act (TCJA) of 2017, which are scheduled to expire.

Who will be most affected by these QBI changes?▼

Changes to the QBI deduction will most directly impact pass-through entities like S corporations, partnerships, and sole proprietorships, as their tax liabilities are tied directly to this deduction.

How can businesses prepare for these changes?▼

Businesses can prepare by reviewing their current tax planning, adjusting business structures, and implementing forecasting and modeling techniques to anticipate different potential scenarios.

What role do tax professionals play in this process?▼

Tax professionals offer essential guidance by providing tailored advice, ensuring compliance, and helping businesses navigate complex tax regulations, optimizing their tax strategies for the future.

Conclusion

As 2025 approaches, understanding and preparing for the proposed changes to the Qualified Business Income (QBI) deduction is crucial for pass-through entities. These entities must proactively engage in tax planning, seek expert guidance, and implement long-term financial strategies to mitigate potential risks and capitalize on opportunities.