ACA 2026 Update: New Subsidies & Enrollment Periods Explained

The 2026 Affordable Care Act (ACA) update brings significant changes to health coverage, including enhanced subsidies and extended enrollment periods, aiming to make healthcare more accessible and affordable for millions of Americans.

Por: Marcelle em 27 de março de 2026

Última atualização em: junho 22, 2026

Anúncios

The 2026 Affordable Care Act (ACA) update introduces crucial changes, including enhanced subsidies and adjusted enrollment periods, designed to improve healthcare accessibility and affordability for eligible Americans nationwide.

Are you ready to navigate the complexities of your health insurance options for the upcoming year? The 2026 Affordable Care Act (ACA) Update: Understanding New Subsidies and Enrollment Periods is poised to bring significant changes that could directly impact your access to affordable healthcare. Staying informed about these crucial adjustments is key to making the best decisions for yourself and your family.

Decoding the 2026 Affordable Care Act Landscape

The Affordable Care Act, commonly known as Obamacare, has been a cornerstone of health policy in the United States since its inception. For 2026, several critical modifications are set to take effect, primarily focusing on enhancing affordability and streamlining the enrollment process. These changes reflect ongoing efforts to address healthcare costs and expand coverage to more Americans.

Understanding the nuances of these updates is not just about compliance; it’s about leveraging opportunities for better, more affordable health coverage. The ACA’s framework is designed to provide a safety net, and the 2026 adjustments aim to strengthen that net, particularly for low and middle-income households. This section will delve into the foundational aspects of these changes and what they mean for the average consumer.

Anúncios

Key Legislative Adjustments for 2026

Increased Subsidy Availability: More individuals and families will qualify for financial assistance.

Expanded Income Thresholds: Eligibility for premium tax credits will extend to higher income levels.

Enhanced Plan Offerings: A broader range of plans may become available on the marketplaces.

The overarching goal of the 2026 ACA update is to reduce the financial burden of health insurance premiums and out-of-pocket costs. By making healthcare more attainable, policymakers hope to decrease the uninsured rate and improve public health outcomes across the nation. These legislative adjustments are a direct response to evolving economic conditions and the persistent demand for equitable healthcare access.

Ultimately, navigating the 2026 ACA landscape requires a proactive approach. Familiarizing yourself with the updated regulations and understanding how they apply to your specific situation will be vital. This foundational knowledge will empower you to make informed choices when the enrollment periods arrive.

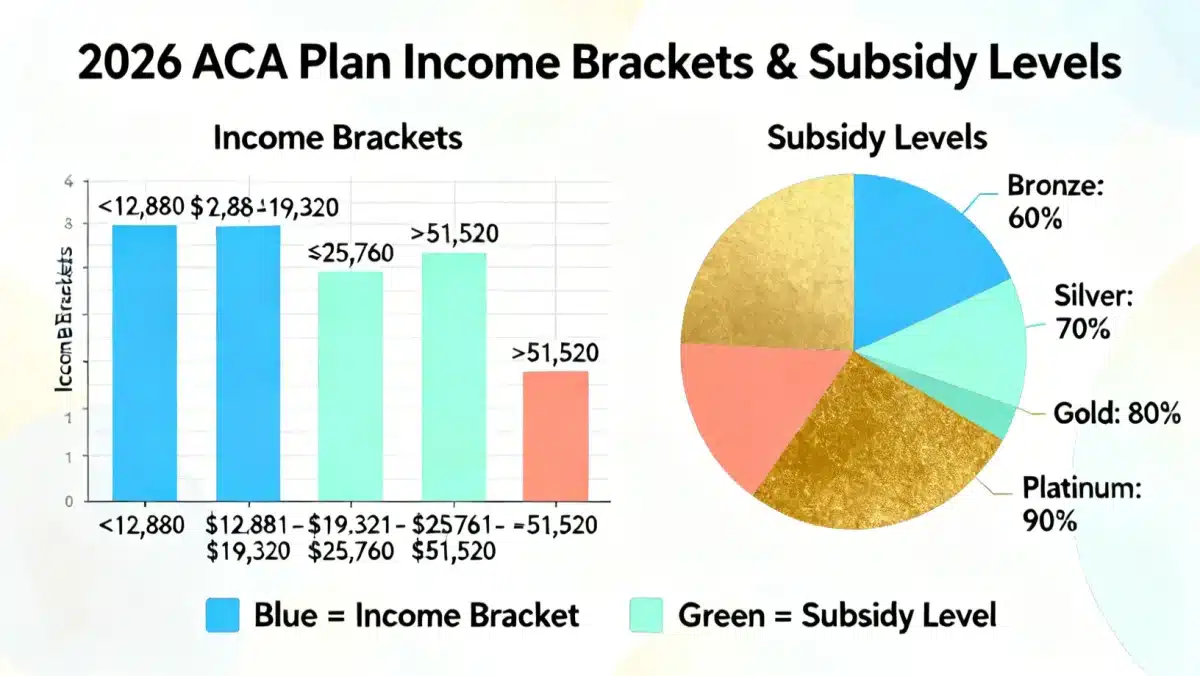

Understanding the New Subsidy Structures and Eligibility

One of the most impactful components of the 2026 ACA update involves significant revisions to the subsidy structures. These financial aids, primarily in the form of premium tax credits, are crucial for making health insurance affordable for millions. The upcoming changes are designed to expand eligibility and increase the amount of assistance available, thereby reducing the net cost of coverage for many.

Previously, subsidy eligibility was capped at 400% of the federal poverty level (FPL). However, the 2026 updates are set to remove this income cliff, meaning that even those with incomes above this threshold may still qualify for some level of assistance if their premiums exceed a certain percentage of their household income. This is a game-changer for many middle-income families who previously found themselves priced out of affordable plans.

How Premium Tax Credits Will Be Calculated

The calculation of premium tax credits will continue to be based on a sliding scale, ensuring that those with lower incomes receive greater assistance. However, the percentage of income individuals are expected to contribute towards their premiums will be adjusted downwards across various income brackets. This means that for the same income level, individuals will likely pay less out of pocket for their monthly premiums compared to previous years.

Income-Based Sliding Scale: Your household income relative to the Federal Poverty Level (FPL) determines your subsidy amount.

Benchmark Plan Consideration: Subsidies are typically based on the cost of the second-lowest-cost silver plan in your area.

Advanced Payments: You can choose to have your tax credits paid directly to your insurer each month, lowering your premium upfront.

It’s important to remember that these subsidies are reconcileable at tax time. If your income changes throughout the year, it’s crucial to update your information on the marketplace to avoid owing money back or missing out on additional credits. The new structures aim to provide more flexibility and support, but accurate reporting remains vital.

Ultimately, the enhanced subsidy structures for 2026 represent a significant step towards achieving universal healthcare access. By making insurance more financially accessible, the ACA continues to evolve, adapting to the economic realities faced by American families. Understanding these new rules is the first step toward securing more affordable health coverage.

Navigating the 2026 Open Enrollment Periods

The open enrollment period is the designated time each year when individuals can sign up for, re-enroll in, or change their health insurance plans through the ACA marketplace. For 2026, while the core concept remains, there might be subtle adjustments to the specific dates and outreach efforts. Being aware of these periods is absolutely critical, as missing them can mean waiting an entire year to get coverage, unless you qualify for a special enrollment period.

Typically, the open enrollment period begins in early November and extends into January of the following year. It is during this window that you can compare plans, assess your subsidy eligibility, and make informed decisions about your health coverage. The 2026 period is expected to follow a similar timeline, but always confirm the exact dates with official sources like Healthcare.gov or your state’s marketplace.

Key Dates and Deadlines to Remember

While specific dates will be officially announced closer to the period, it’s wise to mark your calendar for the typical timeframe. Early preparation allows for thorough research and avoids last-minute rushes. Pay close attention to deadlines for coverage starting on January 1st, as these usually fall in mid-December.

Start Date: Generally, early November.

Deadline for January 1st Coverage: Mid-December.

End Date: Typically, mid-January of the following year.

Remember that if you already have a marketplace plan, it will often automatically re-enroll you in a similar plan if you do not actively make a change. However, this automatic re-enrollment might not be in your best interest, as plans and subsidies change yearly. It’s always recommended to actively review your options to ensure you have the most suitable and cost-effective coverage.

Navigating the open enrollment periods effectively ensures continuous and appropriate health coverage. By staying informed about the start and end dates, and by actively engaging with the marketplace, you can secure the best possible plan for your needs and budget for 2026.

Special Enrollment Periods: What You Need to Know

Beyond the standard open enrollment period, certain life events trigger what are known as Special Enrollment Periods (SEPs). These periods allow individuals to enroll in or change their health insurance plans outside of the regular open enrollment window. The 2026 ACA update does not significantly alter the qualifying life events for SEPs, but understanding them remains crucial for anyone experiencing significant life changes.

SEPs are designed to ensure that individuals and families can maintain continuous health coverage during times of transition. Without SEPs, someone who loses job-based insurance mid-year, for example, would be left without options until the next open enrollment period, potentially leading to gaps in critical healthcare access.

Qualifying Life Events for SEPs

A range of circumstances can qualify you for a Special Enrollment Period. These events typically involve changes in your household, residence, or loss of existing health coverage. It’s important to report these changes promptly to the marketplace, usually within 60 days of the event, to activate your SEP.

Changes in Household: Marriage, divorce, birth or adoption of a child, or death in the family.

Changes in Residence: Moving to a new county or state that offers different health plans.

Loss of Health Coverage: Losing job-based insurance, COBRA expiration, or aging off a parent’s plan.

Changes in Eligibility for Assistance: Becoming newly eligible for subsidies.

It is vital to provide documentation to verify your qualifying life event when applying through a SEP. The marketplace will require proof of the event, such as a marriage certificate or a letter from your previous employer confirming loss of coverage. Failure to provide timely and accurate documentation can delay or prevent your enrollment.

Understanding the conditions that trigger a Special Enrollment Period is a key aspect of maximizing your ACA benefits. These provisions offer a vital safety net, ensuring that life’s unexpected turns do not leave you without essential health coverage. Always keep track of significant life changes and consult the marketplace for guidance on your eligibility.

Impact of the 2026 ACA Updates on Specific Populations

The 2026 ACA updates are not uniform in their impact; certain demographic and economic groups are likely to experience more pronounced effects. Understanding these differential impacts can help individuals and policymakers better prepare for the changes. The primary beneficiaries are expected to be low and middle-income families, as well as those living in areas with limited plan competition.

For individuals residing in states that have expanded Medicaid, the federal poverty level calculations for subsidy eligibility will continue to interact with Medicaid thresholds. This means that some individuals may transition between Medicaid and marketplace plans with subsidies, depending on their income fluctuations. The aim is to create a more seamless transition and prevent coverage gaps.

Targeted Benefits for Low-Income Households

The elimination of the income cliff and the enhancement of premium tax credits are particularly beneficial for low-income households. These changes mean that a smaller percentage of their income will be required for health insurance premiums, freeing up financial resources for other necessities. This can significantly reduce financial strain and improve overall well-being.

Reduced Premium Burden: Lower out-of-pocket costs for monthly premiums.

Access to Higher-Quality Plans: Increased affordability might allow selection of plans with lower deductibles or better benefits.

Improved Health Outcomes: Consistent access to care due to reduced financial barriers.

For middle-income families, the removal of the 400% FPL income cap for subsidies is a significant relief. Many families in this income bracket previously faced substantial premium costs without any financial assistance. The 2026 changes are designed to ensure that no family pays more than a certain percentage of their income for health insurance, regardless of how far above the FPL they are.

The 2026 ACA updates represent a targeted effort to improve health equity. By focusing on affordability and accessibility for vulnerable populations, the changes aim to create a healthcare system that is more responsive to the diverse needs of American citizens. These impacts will likely be observed in improved enrollment rates and better health outcomes across the board.

Maximizing Your Benefits: Tips for 2026 Enrollment

With the 2026 ACA updates on the horizon, taking proactive steps to maximize your benefits is more important than ever. The changes to subsidies and enrollment periods offer new opportunities, but navigating them effectively requires careful planning and informed decision-making. Don’t wait until the last minute to explore your options.

One of the most crucial tips is to start your research early. Even before the official open enrollment period begins, you can familiarize yourself with the types of plans available in your area, understand the general subsidy guidelines, and gather necessary documentation. This preparation will make the actual enrollment process much smoother and less stressful.

Essential Steps for a Smooth Enrollment

Estimate Your Income Accurately: Your projected household income for 2026 is critical for subsidy calculations.

Compare Plans Thoroughly: Look beyond just the premium; consider deductibles, out-of-pocket maximums, and network providers.

Utilize Free Assistance: Take advantage of navigators and certified enrollment counselors available through the marketplace.

Another key strategy is to update your information on the marketplace even if you are re-enrolling in an existing plan. Your household size, income, or even your address might have changed, which could impact your eligibility for subsidies or the plans available to you. Regular updates ensure you are always receiving the correct amount of financial assistance.

Finally, consider the long-term implications of your chosen plan. While a low premium might seem attractive, a high deductible could lead to significant out-of-pocket costs if you require extensive medical care. Balance immediate savings with potential future expenses to select a plan that truly meets your healthcare needs and financial situation for 2026.

Anticipated Challenges and Future Outlook for ACA

While the 2026 ACA updates bring considerable improvements, it’s also important to acknowledge potential challenges and consider the future outlook of the Affordable Care Act. Healthcare policy is dynamic, and ongoing discussions about funding, political support, and implementation will continue to shape the ACA’s trajectory. Understanding these potential hurdles can provide a more comprehensive perspective.

One challenge could be ensuring that all eligible individuals are aware of the new subsidies and enrollment opportunities. Despite outreach efforts, a significant portion of the population might remain uninformed, leading to missed opportunities for affordable coverage. Effective communication and public education campaigns will be crucial to maximize the impact of these updates.

Potential Hurdles in Implementation

The administrative burden on state and federal marketplaces to implement the new subsidy calculations and manage increased enrollment volumes could also pose a challenge. Ensuring that systems are robust enough to handle the influx of applicants and accurately process financial assistance will be vital for a smooth rollout. Technical glitches, though hopefully minimal, can always occur.

Awareness Gap: Ensuring all eligible individuals know about new benefits.

Administrative Capacity: Marketplaces must handle increased demand efficiently.

Political Volatility: Ongoing debates about healthcare reform could influence future changes.

Looking ahead, the future of the ACA will likely involve continuous refinement. As healthcare costs evolve and new medical technologies emerge, the act will need to adapt to remain relevant and effective. Debates over public health insurance options, drug pricing, and preventative care are expected to continue, potentially leading to further legislative adjustments beyond 2026.

Despite these challenges, the 2026 updates represent a significant commitment to strengthening the ACA and expanding access to affordable healthcare. The long-term outlook suggests a continued focus on addressing cost barriers and ensuring that more Americans have the health coverage they need to thrive. Staying engaged with policy discussions will be key to understanding future developments.

Key Point

Brief Description

Enhanced Subsidies

Increased financial assistance for premiums, extending to higher income levels by removing the 400% FPL cap.

Open Enrollment

Annual period for plan selection or change, typically from early November to mid-January, with specific dates to be confirmed.

Special Enrollment Periods

Opportunities to enroll outside open enrollment due to qualifying life events like marriage, birth, or loss of existing coverage.

Impact on Populations

Significant benefits for low and middle-income families, with more affordable premiums and broader access to plans.

Frequently Asked Questions About the 2026 ACA Update

What are the main changes in the 2026 ACA update?▼

The primary changes for the 2026 ACA update include enhanced premium tax credits, making health insurance more affordable for a wider range of income levels. Additionally, there are potential adjustments to the open enrollment periods and continued emphasis on special enrollment opportunities for qualifying life events.

How will the new subsidies impact my monthly premiums?▼

The new subsidy structures aim to reduce the percentage of your income you pay towards health insurance premiums. For many, this means lower monthly out-of-pocket costs, especially for middle-income households who previously didn’t qualify for assistance. Your exact savings will depend on your household income and local plan costs.

When is the 2026 open enrollment period?▼

While official dates are usually announced closer to the period, the 2026 open enrollment is expected to run from early November 2025 to mid-January 2026. It is crucial to check Healthcare.gov or your state marketplace for the precise dates to ensure you don’t miss the deadline for coverage.

Can I still get coverage if I miss open enrollment?▼

Yes, you may still be able to get coverage through a Special Enrollment Period (SEP) if you experience a qualifying life event. These events include marriage, divorce, birth of a child, moving to a new area, or losing other health coverage. You typically have 60 days from the event to apply.

Where can I find help understanding my ACA options?▼

You can find free assistance through navigators and certified enrollment counselors. These experts are available through the ACA marketplace (Healthcare.gov) or local community organizations. They can help you understand plan options, calculate subsidies, and complete the enrollment process effectively for 2026.

Conclusion

The 2026 Affordable Care Act (ACA) update represents a significant evolution in American healthcare policy, primarily aimed at enhancing affordability and accessibility for millions. With new subsidy structures and potentially adjusted enrollment periods, individuals and families have a renewed opportunity to secure comprehensive health coverage that fits their budget. Staying informed, actively engaging with the marketplace, and utilizing available resources are crucial steps to maximizing the benefits offered by these changes. As healthcare continues to adapt, the ACA remains a vital tool in ensuring that more Americans have access to the care they need, fostering a healthier and more secure future for all.